Buy Argent Energy

March 18, 2014

On November 24, 2013 CymorFund recommended Argent Energy at $7.97. Since then Argent Energy Trust has fallen dramatically and closed yesterday at $5.37. In the interim, it has distributed dividends of $0.43, making a net loss since of $2.17, or 27%.

The fall off has been dramatic, and this large loss has hurt our performance numbers substantially. In spite of this loss, our performance is still over 22% for the the first 2 months of 2014, and for the year 2014 to date. Had Argent Energy performed normally, our performance numbers would have been much higher.

What Happened to Argent Energy Trust?

There have been no dramatic events to warrant this dramatic fall in value. Everything appears to be performing as expected. We republish a press release from the company dated March 7, 2014 in which management appears mystified by this fall in value. We also republish below the press release detailing the results of 2013.

We intend on seeing company management shortly and will report anything of note.

News Release of March 7, 2014

Argent comments on recent market activity

CALGARY, March 7, 2014 /CNW/ – Argent Energy Trust (“Argent” or the “Trust”) (TSX: AET.UN) notes that there continues to be high trading volume and price volatility in Argent units over the past few days, which may be related to recent analyst reports. On March 5th, 2014, the Trust released its year-end December 31, 2013 audited financial statements and management’s discussion and analysis thereon, and there are no other material items to be disclosed.

The Trust believes that its expected funds flow from operations and the availability under its long term bank credit facility (being only US$90 million drawn on its US$160 million facility), together with DRIP program, will be sufficient to fund its working capital, its current capital investment program, enable it to meet all current and expected financial requirements, including interest payments and maintaining Unitholder distributions.

Furthermore, Management of the Trust reiterates that its net asset value per unit at December 31, 2013, based on independent third party audited data, is $7.93.

News Release of March 4, 2014 Reporting Year End and last 3 months Performance – Very Positive

Highlights for the three months and year ended December 31, 2013

Operations

- Completed first full year of operations, growing from approximately 1,600 boe/d barrels of oil equivalent (“boe/d”) (36% oil and NGLs) at IPO on August 10, 2012 , to an average of 6,975 boe/d (68% oil and NGLs) for December 2013 .

- Q4 2013 funds flow from operations increased to $18.3 million , or $0.31 per Unit, from $7.4 million , or $0.21 per Unit in Q4 2012. For the year ended December 31, 2013 , funds flow from operations was $64.6 million , or $1.22 per Unit. The increase in funds flow from operations was mainly due to higher production and higher netbacks, as the Trust brought new, mainly oil wells on production and acquired oil & gas properties during 2013.

- Q4 2013 loss was $82.7 million , or $1.39 per Unit, as compared to Q4 2012 income of $270,000 , or $0.01 per Unit. Year-ended December 31, 2013 loss was $87.2 million , or $1.65 per Unit. This loss arises mainly due to non-cash charges in Q4 2013, including a $69.2 million impairment related to Texas unconventional (primarily on Austin Chalk probable reserves) and Oklahoma oil assets (primarily on probable reserves in one field), and $8.4 million in increased depletion charges arising from changing to using proved reserves as depletion basis instead of proved plus probable reserves.

- Q4 2013 oil & gas sales increased by 140% to $44.1 million , as compared to $18.4 million in Q4 2012. For the year ended December 31, 2013 , total oil & gas sales before royalties and risk management gain or loss were $154.4 million .

- Average production in Q4 2013 increased by 113% to 6,747 boe/d (71% oil and NGLs) from 3,169 boe/d (57% oil and NGLs) in Q4 2012, reflecting new, mainly oil wells coming on production and the acquisition of oil weighted properties during 2013. For the year ended December 31, 2013 , the average production was 5,591 boe per day (69% oil and NGLs).

- Netbacks from sales volumes for Q4 2013 were $21.3 million , or $34.33 per boe, while for the year ended December 31, 2013 netbacks from sales volumes were $74.7 million , or $36.68 per boe.

Financing

- During 2013, the Trust obtained an increase in the credit limit of its long term credit facility to US$160 million as at December 31, 2013 . Of this facility, only US$77 million was drawn at year end.

- Declared unitholder distributions of $1.05 per Unit during 2013 ( $0.0875 per Unit per month).

An Opportunity – a 20% ROI

Making money in the market depends more on timing than on choosing the right stocks. If you read Warren Buffet, or the many blogs we have published advising readers of how important timing is, the consistent theme is that buying at the right time is the most important factor in whether investments make money. As Mr Buffet says “Price is what you pay. Value is what you get.” In other words, what you pay depends on when you buy.

Argent Energy Trust today pays a dividend of $0.0875 per share. This is an annualized distribution of $1.05 per trust unit which represents a cash-on-cash yield of approximately 19.56%.

For a well run company, this enormous yield indicates that the share price is very undervalued currently.

Our Original Recommendation is Reprinted Below

Cymorfund Stock Pick: Argent Energy Trust (TSX-AET.UN $7.97)

November 24, 2013

A Play on Words

Today’s CymorFund 10-Bagger Investment Letter stock pick is Argent Energy Trust. The word Argent can be a French word, which translates to Tincture of Silver in English, which is a precious metal. This company is surely a precious ‘thing’.

Our new stock pick is a bit of a hybrid of a company. It isn’t in Our 10Bagger category, but it is a short term large profit, a long term nice dividend yield, and a great way to make money.

Income Trusts

In the early 2000’s, Income Trusts proliferated in Canada and were a corporate entity that allowed the flowthrough of their earnings directly to their shareholders without those earnings being taxed at the corporate level. This type of corporate structure traded like a stock on the public markets, but distributed its income to its unit-holders. The purpose of these Income Trusts was to encourage gas and oil exploration and development.

The thought was that so long as the profits were taxed at some level, the eventual net revenue to the government would be the same. This type of company was called an “Income Trust“, and was designated on the public markets in Canada by the letters”.UN” placed after the trading symbol..

Enterprising entrepreneurs realized that the Income Trust structure could be of interest to investors in many different industries, and was an ideal type of corporate structure to attract investors. As more and more companies converted to being Income Trusts (due to the favorable tax treatment, and the high valuation that investors put on their shares, because in effect there was no income tax paid at the corporate level) the government became alarmed and mandated the end of Income Trusts except in certain specialized industries. most commonly known in the real estate industry as REITs (Real Estate Investment Trusts).

Energy Trusts

Another exception to the end of Income trusts were Energy Trusts that held all of their assets outside of Canada. Argent Energy Trust is such a Energy Trust. It remains elligible to distribute its profits directly to its unitholders. Currently Argent Energy Trust has a 14% yield, which is quite spectacular, and well worth looking at.

The question is whether this company has good assets, is sustainable, and is currently a bargain.

A Unique Opportunity to Profit

Argent Energy Trust recently reported that it drilled a dry hole in Texas. When it announced this news, the market immediately punished the stock. Few traders in the market take the time to understand the nuances and background behind events. They restrict themselves to glancing at the headlines and reacting immediately.

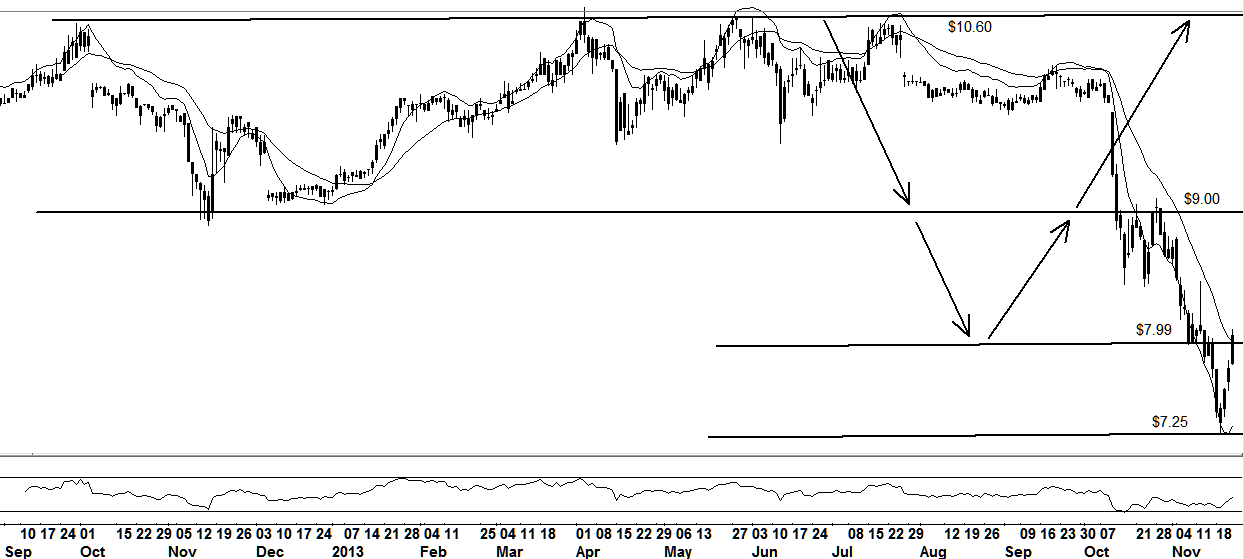

The stock plummeted . The following chart shows the event. The stock went public in the fall of 2012 at $10.00. It traded up, and then down, and eventually settled around the $10.00 range. When the news hit in October 2013, the stock dropped $2.00 and continued falling to almost a low of $7.15. Now investors have started to realize that the event was wildly overblown, and in a matter of days the stock has recovered to almost $8.00

What Really Happened

AET.UN had the opportunity to obtain a significant increase in their land position, in an area that is extremely prospective. To fulfill their contractual obligation to gain permanent rights over these lands, they were required to spend a certain amount of money and drill a well. They chose a location and fulfilled this obligation.

The well was dry – it did not produce economic amounts gas or oil. What this meant was that particular well was dry, but the land is now theirs and there are many prospective areas to be drilled that the company believes to have large potential. What compounded the problem was that the company was in a ‘blackout’ period, where insiders were aware of pending news and under TSX and all market regulations, the company was prohibited from public announcements.

We Are In The Age of Instant Communication

The result was that the internet blogs, bullboards and chat rooms picked up on the fact of the dry well, and the fact that the company was being silent, and rumors spread rapidly. In the absence of information, fear and paranoia spread instantly in this age of instant communication. As fast as the rumors spread, investors dumped the stock.

Of course the Age of Instant Information does not relate to the speed of archaic rules of investor governance. False information can destroy stock values in an instant. It is well known that whatever the cause, a stock always drops much more precipitously than it recovers. Recovery takes longer.

Argent Energy is Stronger Than Ever

As at November 2013, AET.UN is producing 7,100 boed, which is a record level. Its cash flow is at a record high. The majority of its production is oil, rather than gas, which makes the profits far greater. They now have a far greater land position than they had before the dry well. With their massive profits, they are able to easily absorb the cost of a dry well without affecting in any significant way the company’s cash position or profits.

When to Buy Stocks

The stock market is a funny place, and the one thing you can be sure of is that it is often not fairly valued, in spite of what the theorists may think. The time to make profit is when a stock is undervalued. AET.Un is very undervalued currently. If you examine the chart, there are a bunch of long established patterns that foretell on a technical basis, what is likely to happen. Follow the arrows that I have positioned on the chart, and all technical indicators say that the likelihood is that the stock will recover to the $10.60 line of resistance/support.

From today’s price, that is a movement of approximately $2.61, which would be a gain of 33 1/3%. A very nice gain in a short period.

The line of resistance/support, mean that that price is a type of barrier to the stock moving higher. When a stock is rising as fast as this one is, that resistance line, often turns into a support line, and the upside from the former line of resistance is usually an equal distance above that line, to what the stock was below that line. In an ideal world, that would be approximately another $3.00 which would value the stock at $13.60. Should this level be reached, the dividend yield would still be a respectable 7.7%, so this possible high point is not out of reach. That would mean a gain from today’s price of $5.61 + a dividend of say 7% during only part of a year, making a total possible gain of $6.30 or almost 80%.

What is Argent Energy Trust

“Argent is a mutual fund trust under the Income Tax Act (Canada). Argent’s objective is to create stable, consistent returns for investors through the acquisition and development of oil and natural gas reserves and production with low risk exploration potential, located primarily in the United States.”

AET.UN’s assets are are oil and gas resource properties and producing or prospective wells in the Southern central USA areas of Texas, Oklahoma, Kansas and Wyoming.

- The principal properties are in the Eagle Ford Shale,

- stable low decline oil fields in all four states, and

- low cost natural gas in South and Central Texas.

- 65% is oil, 5% is NGL, and 30% is natural gas.

- For 2013, 91% of its Estimated Total Revenue will be derived from oil.

- It is the operator of over 93% of its oil and gas production and

- controls where it drills, what it drills, and its own cash flow.

- Its properties have a stable long life reserve base averaging approximately 17 years.

Regardless of a dry well, this company will be profitable and paying dividends for many years to come.

Has There Been a Real Change in the Company’s Operations?

The following is a quote from the company’s latest press release dated November 18. 2013. The press release was issued as a result of the stock price volatility previously described here.

“Argent unitholders can be assured that there are no material operational or financial events impacting the Trust’s business beyond what has previously been disclosed. Argent’s current 30 day production average is over 7,100 boe/d (72% Oil and NGLs) and it remains on track to achieve its 2013 average annual production guidance of 5,700 boe/d and 2013 exit production guidance of approximately 7,000 boe/d. Furthermore, Argent’s current distribution level remains intact and the Trust has no plans to reduce the level of distribution.”

What this means is that the market – as usual – has wildly over reacted to news without understanding the news, and as a result created an opportunity for us to make some very nice money on this stock.

Financials

- market cap of about $475 million

- about 59 million shares

- available credit facilities of $160 million

- currently using $78 million of this credit facility

- available existing losses for income taxes about $590 million to offset future income taxes

- average 2013 production approx 5,700 boed

- ending 2013 with a massive increase to 7,100 boed

- reserve life index 17 years

- estimated 2P reserves 42 MMBOE

- Additional existing potential 40 MMBOE

- existing 230 drilling locations

Dividends

- monthly

- $0.088 per share

- current annual yield between 14% and 14%

Fiscally Conservative and Ideally Positioned

The company’s properties and production are located close to transportation and close to shipping ports and distribution points. Its cost of transport does not include long distances through expensive pipelines, and it makes more per barrel than its more distant competitors

It is financially conservative and hedges the majority of its production, thereby locking in current prices.

- up to 70% of its royalty forcasted production for the next 12 months are hedged

- up to 60% going 24 months forward

- up to 50% going 36 months forward

Risks

The largest risk is the ever increasing supply of domestically produced oil and gas, which some predict will drive the price of these commodities lower. AET.UN has somewhat mitigated that risk short term by hedging forward its production as much as 36 months. Yet markets often anticipate future problems and drive stocks down well in advance of problems occurring.

Buy Argent Energy Trust (TSX- AET.UN $7.97)

The risk/reward ratio is very favorable now. If you want a nice reward, buy now. If you want a long term dividend, revisit the situation in a year and see if the dividend remains attractive after the stock has risen.

While this website and the author’s opinions, are intended to be as accurate as possible, the information contained herein is based on sources which we believe reliable but is not guaranteed as being accurate or a complete statement or summary of the available data. We assume no responsibility for errors, omissions, or contrary interpretation of the subject matter herein. Any perceived slights, omissions, or mis-statements of specific persons, peoples, or organizations other published materials are unintentional.

This information is not intended for use as a source of legal, business, accounting or financial advice. All readers are advised to seek services of competent professionals in the respective fields. No representation is made or implied that the reader will do as well from using the suggested techniques, strategies, methods, systems, or ideas; rather it is presented for news value only. We do not assume any responsibility or liability whatsoever for what you choose to do with this information. Use your own judgment. There are no guarantees.

We may or may not have positions in securities we name. In making an investment decision consider numerous factors such as portfolio balancing, timing, cash and capital reserves, asset allocation and other. Do your own research. Matters discussed contain forward-looking statements that are subject to risks and uncertainties and actual results may differ materially from any future results, performance or achievements expressed or implied.

Views expressed are opinions and not investment advice. You should retain a licensed professional to guide you and not rely on the opinions expressed herein. This report is neither a solicitation nor a recommendation to buy or sell securities. We are not a registered investment advisor nor a broker-dealer. Any perceived remark, comment or use of organizations, people mentioned and any resemblance to characters living, dead or otherwise, real or fictitious, is purely unintentional and used as examples only.